Colorado · USA

From a ski-in/ski-out chalet in Aspen's West End to a mountain lodge above Vail's Back Bowls — fractional ownership in Colorado means a deeded share of North America's most celebrated high-altitude second-home market, six to seven weeks of personal use a year, and a fully managed home at altitude waiting whenever you arrive.

20 properties · from $620,000

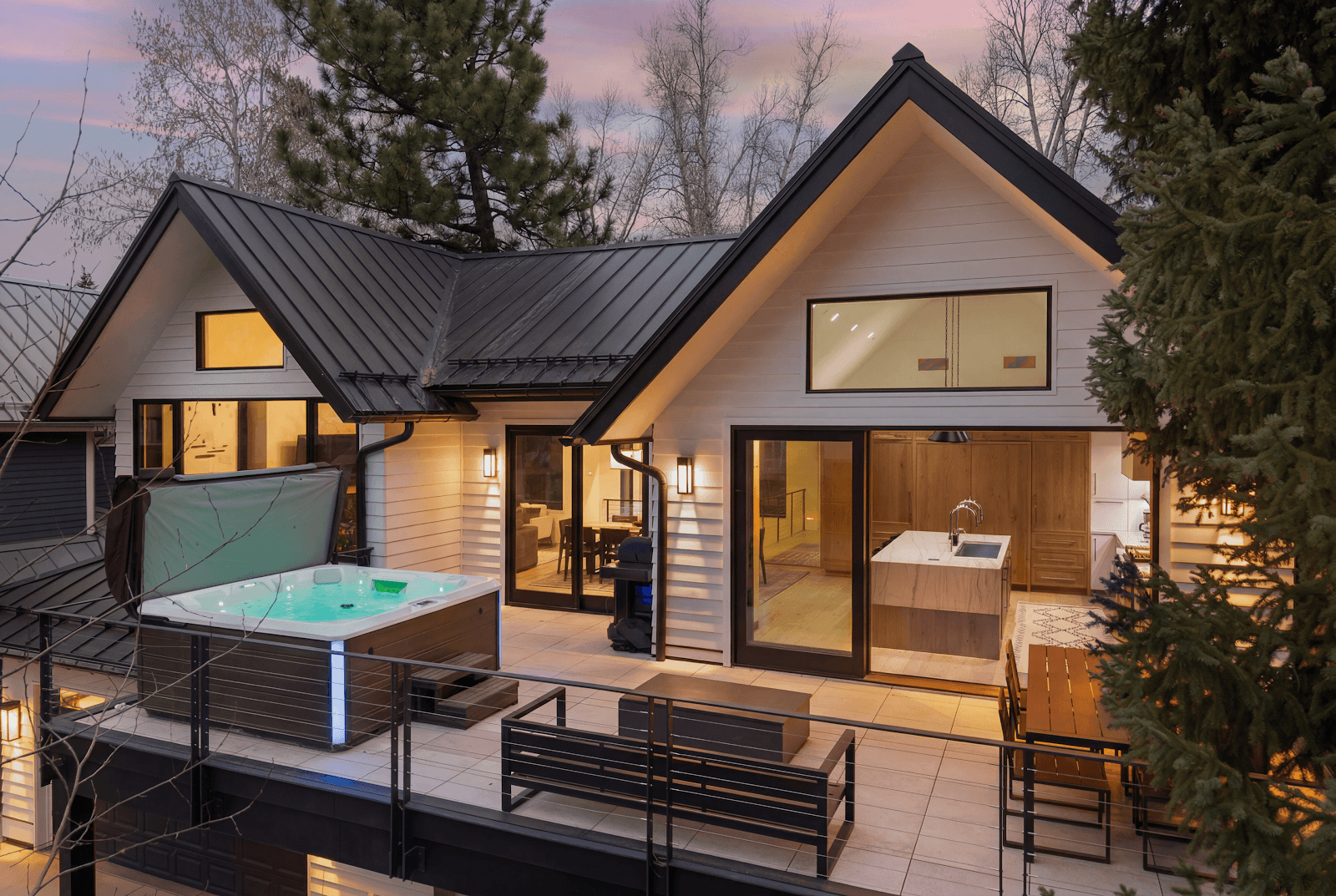

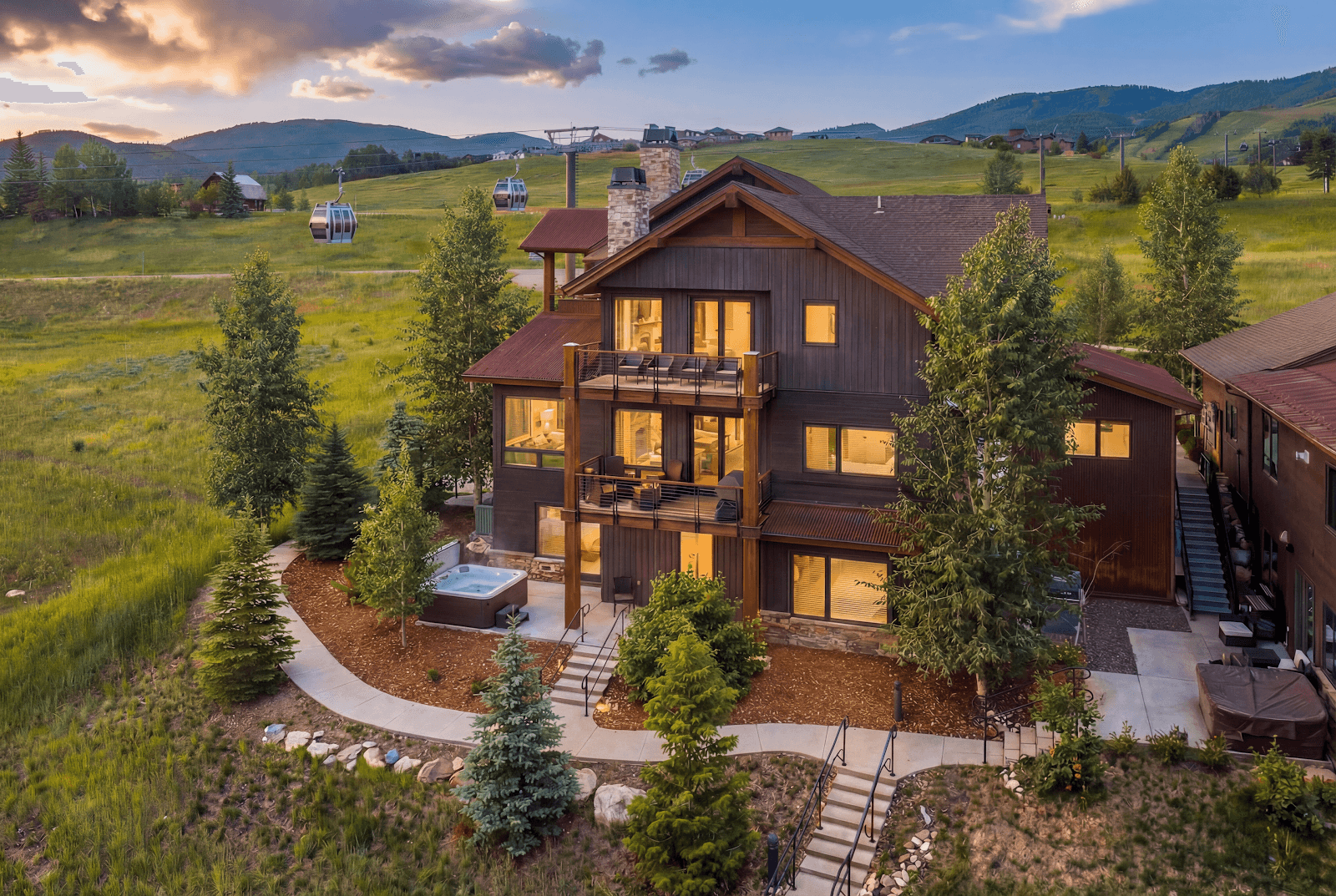

Fully managed ski chalets, mountain lodges and alpine homes across Aspen and Snowmass Village, Vail and Beaver Creek, and Breckenridge and Summit County. Your 1/8 deeded share comes with 6–7 weeks of personal use, a professional management team on call, and the long-term equity of North America's most supply-constrained high-altitude second-home market.

Fractional ownership in Colorado means buying a deeded 1/8 share of a luxury high-altitude second home — held in a purpose-built LLC alongside up to seven other co-owners. Each owner receives approximately 45 days of personal use per year through a fair-rotation calendar, with all property management, maintenance, taxes and operations handled by a professional team. It is real, recorded property equity in your name — not a timeshare, not a holiday club.

Colorado is, by almost any serious measure, the premier mountain second-home market in North America. The state's Rocky Mountain corridor stretches roughly 200 km (125 miles) west and south-west of Denver International Airport — the single most important logistical fact in the market — anchored by a sequence of resort towns that have accumulated over six decades of ski-resort investment, real-estate development and international-buyer infrastructure unmatched anywhere else on the continent. Aspen, Vail, Breckenridge, Steamboat Springs, Telluride, Beaver Creek — each name is both a geographic location and a brand identity built through decades of deliberate development, and together they constitute the world's most globally recognised cluster of high-altitude leisure real estate outside the French and Swiss Alps. Colorado's snowpack is among the most reliable on earth: the state's high-elevation continental climate produces the crystalline, low-moisture snow the region famously calls "the Colorado powder," with annual accumulations at the major resorts typically running to 7–10 m (23–33 ft) in the deepest snowpack years, and average ski seasons extending from late November through mid-April — a longer reliable window than many European comparables at lower altitude. The Colorado Department of Transportation maintains the mountain corridors as a primary infrastructure priority, with I-70 upgraded to handle the Denver-to-mountains weekend flow at a scale no other US mountain state has matched.

Your Colorado share is held inside a purpose-built LLC alongside up to seven other co-owners. This is the same modern international structure used across every property on COP — the United States, the United Kingdom, France, Spain, Italy and elsewhere — rather than a jurisdiction-specific vehicle that varies country by country. The practical effect for a Colorado buyer is immediate. Your ownership runs through one consistent structure regardless of which COP destination you own in; transferring an LLC membership interest is a more direct administrative action than triggering a full Colorado real-estate title conveyance through a county recorder's office; and for the growing cohort of owners pairing a Colorado ski share with a Mediterranean or European summer share, the consistency of the LLC framework across both means you handle one model rather than two or three different vehicles. For buyers already familiar with Colorado's robust property-law tradition — Colorado has been recording real estate transactions at the county clerk and recorder for over 150 years — the LLC structure sits naturally within that framework while adding the efficiencies of a shared international corporate vehicle.

The second structural argument for Colorado is the combination of summer and winter quality that sets it apart from purely seasonal European ski destinations. Colorado's resort towns are not one-season addresses. Summer in the Rockies — June through September — delivers some of the finest high-altitude hiking, mountain biking, fly-fishing, white-water rafting and cultural programming available anywhere in North America. Aspen Music Festival, one of the world's great classical music festivals, runs every July and August, drawing international performers and audiences for ten weeks. The Food and Wine Classic in Aspen has been the flagship event of the American food calendar for over four decades. Breckenridge's summer music season runs from the Breckenridge Music Festival through outdoor concerts on the Main Street plaza well into September. Vail's summer mountain biking trails — rated among the best lift-served trail networks in the United States — are at their best in July and August, when the same gondolas that carry skiers in winter carry riders and their bikes to altitude in summer. The practical consequence for a fractional buyer is that a Colorado 1/8 share delivers genuine multi-season usability, with both a winter ski block and a summer mountain or cultural block as viable components of the 45-day annual allocation. This is materially different from a property whose value is purely winter-seasonal — a summer-empty French village chalet, say, or a ski-only property in a one-season Andean destination.

The third structural advantage worth naming explicitly is Colorado's position outside the Schengen Area — and the particular importance of that for British and non-European buyers since the post-2020 Brexit restrictions took effect. UK nationals visiting Schengen-area countries including France, Spain, Italy, Austria and Switzerland are now subject to the 90-day-in-180-day rule, which limits the total number of days spent across all Schengen countries combined in any given 180-day rolling window. A British co-owner holding a Courchevel chalet share cannot make separate trips to Mallorca in the same period without counting against the same 90-day limit. A Colorado share has no such restriction: as a non-Schengen destination, US mountain time does not count against Schengen days, and there is no cap on how long a UK national can stay — the standard visa waiver (via ESTA) allows stays of up to 90 days per trip with no rolling 180-day constraint across the calendar year. For owners who also hold European COP shares, this means their Colorado weeks are genuinely additional days — not drawn from the same pool. This is a practical structural advantage that has become a decisive factor for a growing number of British fractional buyers who were previously exclusively European-mountain focused.

The depth of Colorado's professional services infrastructure for non-resident and international owners is a fourth factor that separates it from almost every other US mountain market and from many European comparables. A state with six decades of resort-property investment has built a deep bench of specialist real-estate attorneys, title companies, CPAs familiar with FIRPTA and international ownership, property managers, HOA professionals and ski-concierge operators across the major resort towns. The institutional knowledge required to operate a mountain second home in a state with snowpack, wildfire-season insurance requirements, altitude-related maintenance considerations and the specific calendar cadences of a ski resort is well-established here in a way that cannot be improvised. The Colorado Division of Real Estate provides a professionally regulated framework for property licensing and the county clerk-and-recorder offices in Eagle, Pitkin, Summit, Routt and San Miguel counties each maintain long-running, reliable public registers for real estate transactions. None of this is glamorous, but it is the kind of institutional depth that determines whether holding a property in a state from another country is a pleasure or a persistent source of administrative friction.

A fifth structural argument — and one that becomes more compelling the more carefully one examines the supply side of Colorado's resort property market — is the genuine scarcity of resort-community land in the major clusters. The towns of Aspen, Vail, Breckenridge and the Snowmass base area sit within or immediately adjacent to either the White River National Forest or adjacent federally administered open-space designations that effectively cap developable land within workable proximity of the ski lifts. Pitkin County's land-use code, shaped by decades of community planning debates since the 1970s growth-control era, produces one of the most restrictive development environments of any US resort county — with strict limits on new floor area, significant affordable-housing requirements for any new construction, and historic-preservation protections that lock the Victorian core of Aspen against significant densification. Eagle County's resort precincts at Vail and Beaver Creek are similarly constrained by the National Forest boundary and the ski area's operating permits. Summit County's Breckenridge is shaped by its own growth management plan and the surrounding Arapaho and Roosevelt National Forests. The consequence is a supply-constrained property market of a kind that is genuinely rare at the scale of Colorado's resort towns: new construction close to the mountain is limited, renovation and redevelopment of existing stock is the primary activity, and the finite inventory of properties in genuinely ski-proximate positions creates durable pricing power for high-quality resort addresses across economic cycles. The Colorado State Demography Office projects continued population growth in the mountain resort counties through mid-century, driven by recreation-focused migration and the expansion of the remote-work economy that has reinforced resort-town demand since 2020 — a structural tailwind for the supply-constrained resort market over the long run. For a fractional buyer, the supply constraint matters directly: the same dynamics that support premium pricing in the whole-ownership market support the fractional market in proportion to the underlying asset. A 1/8 share in a supply-constrained market benefits from the same fundamentals as a whole property at the same address — the land scarcity, the demand depth, the institutional-grade asset quality — at the fractional entry level and with the management overhead transferred entirely.

Colorado's mountain second-home market is best understood through three principal clusters, each with its own architecture, elevation profile, buyer character and price band, plus a set of smaller resort communities that serve specific sub-profiles. The market runs from the hyper-premium Aspen-Snowmass corridor — the world's most globally recognised ski address outside Europe — through the Vail-Beaver Creek axis in Eagle County, which combines the largest certified ski terrain in the US with the elegantly managed Vail Village and Beaver Creek's extraordinary ski-in/ski-out resort environment, down to Breckenridge and Summit County, which packages genuinely world-class terrain, an authentic Victorian Main Street, and the most accessible mountain address from Denver into the most broadly liquid fractional market in the state. Beyond those three, Steamboat Springs offers a more local, less internationalist mountain-town atmosphere in Routt County, and Telluride and Mountain Village in San Miguel County deliver a remotely positioned, architecturally remarkable, deeply supply-constrained alternative for buyers whose priorities run toward privacy and dramatic landscape over logistical ease. The three main clusters are the primary focus for co-ownership buyers and are explored in detail below.

Aspen, the Victorian mining town that reinvented itself as a winter resort in the late 1940s and has since grown into what is arguably the world's most culturally complete ski destination, sits at 2,438 m (7,999 ft) in the Roaring Fork Valley, a further 40 km (25 miles) south-west of Glenwood Springs along the I-70 corridor. The town of Aspen is small — its permanent population runs to under 7,000 — but the cultural infrastructure it sustains is extraordinary. The Aspen Music Festival runs each July and August with over 300 events; the Aspen Institute hosts global policy seminars year-round; the Aspen Art Museum (designed by Shigeru Ban, opened 2014) operates on a New York City gallery model in a Victorian Colorado mountain town; the Food and Wine Classic fills the town for a long weekend every June with the American food world's most concentrated calendar. The skiing itself spans four distinct mountains — Aspen Mountain (the in-town steep-and-expert terrain above the gondola base at Lift 1A on Dean Street), Aspen Highlands (the legendary Highland Bowl, a hike-to expert zone that is among the finest steep skiing in North America), Buttermilk (the gentler family and beginner mountain hosting the ESPN Winter X Games annually), and Snowmass (the largest of the four, with over 3,300 acres across five distinct ski zones including the Elk Camp beginner-and-intermediate network and the Hanging Valley Wall expert terrain). Together the four mountains constitute the Ikon Pass's most prestigious single cluster in North America.

Snowmass Village, 19 km (12 miles) up the road from Aspen proper, is architecturally distinct from its famous neighbour — a planned village built in 1967 that was designed from the start as a ski-in/ski-out resort community rather than an adapted mining town. The base village around the Snowmass Mall and the newer Base Village development combine restaurants, retail and ski-lift access at a more immediate proximity to the mountain than the in-town Aspen experience; the residential offer includes ski-in/ski-out condominiums and townhomes that in other destination contexts would be the most prestigious addresses on the mountain. The international buyer mix in Aspen is the most diverse in Colorado — with consistent representation from the United Kingdom, Germany, Switzerland, France, Brazil, Argentina, Mexico and the broader European and South American markets, alongside the US domestic core of New York, Chicago, Los Angeles and Texas buyers. Best for: buyers who want the most internationally branded mountain address in North America, with year-round cultural depth (music, food, arts, policy) alongside world-class skiing, and who value the cachet and resale liquidity of the world's most recognisable ski-town brand; and buyers for whom the summer cultural and lifestyle seasons are as important as the winter ski season.

Vail sits at 2,457 m (8,061 ft) in the Eagle River Valley, approximately 160 km (99 miles) west of Denver via I-70, and the ski mountain above the town is, by the standards of most informed judges, the finest single ski area in the United States. The Back Bowls — seven named open-terrain bowls totalling over 2,600 acres of ungroomed and groomed skiing on the mountain's south side — are without a clear American equivalent. The Blue Sky Basin extension, added to the Vail ski area in 1999, adds a further 645 acres of tree skiing and open terrain accessible by gondola from the Back Bowls. Total ski terrain covers over 5,300 acres on 195 named trails — the largest certified ski resort in the United States by the National Ski Areas Association's ski-area acreage metric — served by 34 lifts including three high-speed gondolas. Vail Village and its sister pedestrian precinct Lionshead are European-influenced pedestrian villages designed in a Tyrolean architectural vernacular unusual in North America: stone-paved streets, gabled rooflines, a covered bridge over Gore Creek, and a commercial core of upmarket restaurants, galleries, boutiques and ski-rental shops that operates at a standard close to European resort villages. The Vail Symposium runs year-round public programmes; the Betty Ford Alpine Gardens are the highest botanical gardens in the US and open through summer; the mountain's summer trail network is regarded as one of the finest lift-served downhill mountain-bike courses in the country. Vail is owned and operated by Vail Resorts, which also operates Beaver Creek, Breckenridge, Keystone and Park City, and the associated Epic Pass gives access to the global Vail Resorts network.

Beaver Creek, a further 16 km (10 miles) west of Vail on the I-70 corridor, is a different mountain environment again — a purpose-designed, gated resort village opened in 1980 that operates at a deliberately smaller scale than its more famous neighbour. Beaver Creek's 1,832 acres of ski terrain have a more concentrated, intimate character than Vail's expansive back-country; the village base is genuinely ski-in/ski-out at a proximity that few European resorts match, with the lifts leaving from the cobbled village plaza. The resort's signature runs — Steep and Deep terrain off the Rose Bowl, the long groomed cruises off Larkspur Bowl, and the Birds of Prey downhill course (host to the FIS Alpine World Cup) — have made it a favourite of advanced recreational skiers and racing enthusiasts. The buyer mix in Beaver Creek is notably more family-oriented and privacy-focused than Vail's more cosmopolitan village core, with a high proportion of large-chalet owners who value the gated village environment over Vail's more open social scene. The Eagle County corridor — Vail-Beaver Creek combined — is served by the Eagle County Regional Airport (EGE), which receives direct seasonal service from Chicago, Dallas, Houston, Atlanta, Los Angeles, New York and other hubs during ski season, supplementing the year-round Denver option. Best for: buyers who want the finest pure ski-terrain quality in the United States paired with a European-style pedestrian village environment; owners with a strong skiing-as-primary-activity bias who want ski-in/ski-out access on world-class terrain; and buyers drawn to Beaver Creek specifically who want the private, family-focused, gated-village environment alongside the Vail corridor's overall infrastructure depth.

Breckenridge occupies a singular position in the Colorado market: it is the most accessible major resort from Denver (around 140 km / 87 miles via I-70 and Highway 9, or around 1 hour 45 minutes in non-holiday-traffic conditions), the most historically authentic — its Victorian Main Street with its 19th-century mining-era buildings and hundred-plus bars, restaurants and shops is genuinely the most complete surviving Victorian mining town in the Mountain West — and the most broadly accessible in terms of terrain diversity, with five interconnected peaks (Peaks 6, 7, 8, 9 and 10) covering 2,908 acres and 187 named trails across beginner, intermediate and expert terrain. Peaks 6 and 7, added between 2013 and 2015, dramatically expanded the resort's advanced and expert acreage and brought it closer to Vail's total-terrain scale. The Breckenridge Tourism Office documents a town with over 200 days of annual events — summer music festivals, the Breckenridge International Festival of Arts, the extraordinarily popular Breckenridge International Snow Sculpture Championships (January, drawing carving teams from over 20 countries), and a Halloween and October festival season that draws from a broad regional audience. The town's elevation of 2,926 m (9,600 ft) makes it one of the highest-elevation incorporated towns in the United States — a fact that gives its snowpack particular depth and its light-quality a particular clarity, but that can be a genuine acclimatisation consideration for buyers arriving from sea level, particularly in the first 24 hours.

Summit County — the broader county in which Breckenridge sits, sharing borders with Eagle County (Vail) to the west — also contains Keystone and Arapahoe Basin, giving Breckenridge owners practical access to a further 1,700+ acres of terrain without leaving the county. The Summit Stage free bus network connects the Summit County resorts to the town of Frisco, Silverthorne and Dillon — providing a walkable-and-transit lifestyle that makes car ownership less essential here than at the more geographically spread resorts. The Summit County residential sub-zones of particular interest to fractional buyers include the historic Victorian core of Breckenridge Main Street, the ski-in/ski-out gondola-base properties on Park Avenue and Peak 9 Road, and the upper-mountain homes above the town on Wellington Road and the higher residential streets. The international buyer mix in Breckenridge is somewhat more weighted toward domestic US buyers — particularly from the Texas, Denver metro, California and Midwest markets — than the Aspen or Vail international cohort, but with a meaningful and growing British and European presence, partly because the resort's straightforward Denver accessibility and the Epic Pass's Breckenridge access dovetail naturally with Denver International Airport's expanding European route network (London Heathrow, Frankfurt, Reykjavík, Paris, Amsterdam and more). Best for: buyers who want the best terrain-to-accessibility ratio in Colorado; families with children of all skiing ability levels; owners who value the authentic Victorian mountain-town environment as much as the skiing; first-time Colorado fractional buyers for whom the Denver drive-distance is logistically important; and buyers who want strong resale liquidity at an entry point that is more competitive than Aspen or Vail.

Beyond the three principal clusters, Steamboat Springs in Routt County — approximately three hours from Denver via I-70 and US-40 — offers a more local and less internationalist mountain-town atmosphere. The resort is notable for its famous champagne powder, a snow texture produced by the region's particularly dry climate and consistently rated among the lightest in Colorado; the town's famous Strawberry Park Hot Springs provide a year-round outdoor thermal experience unusual even in Colorado's mountain communities; and the two-hour scenic rail heritage route of the Durango & Silverton Narrow Gauge Railroad — accessible as a day trip from Telluride — is one of the state's great heritage experiences. Telluride and Mountain Village in San Miguel County, in the south-west of the state, sit in a dramatically positioned box canyon at 2,667 m (8,750 ft), accessible via Telluride Regional Airport (TEX) or by road over the Lizard Head Pass from the I-70 corridor. The skiing is genuinely world-class — 2,000+ acres, over 1,900 m (6,255 ft) of vertical descent — and the town's cultural calendar, including the Telluride Bluegrass Festival, the Telluride Film Festival, and the Jazz Celebration, is among the most distinctive in any Colorado mountain town. Properties in Telluride and Mountain Village are among the most supply-constrained in the state; fractional buyers drawn to the remoteness and dramatic landscape find fewer competing addresses here than anywhere else in the Colorado resort market. Best for: buyers who prioritise dramatic landscape and genuine remoteness over logistical ease; cultural enthusiasts who treat the Telluride festival calendar as a primary draw; and fractional owners whose existing properties elsewhere mean logistical accessibility is less critical and the distinguishing aesthetic of the box-canyon setting is the central appeal.

Spreading 45 days of use across a Colorado calendar is, in fact, a pleasure — because Colorado is genuinely a twelve-month mountain destination, with each season offering a distinct character that rewards different use patterns. Below is how the year actually unfolds across the portfolio's three main clusters.

Colorado's ski season typically opens at the major resorts from mid-November — Breckenridge and A-Basin often trail-open before Thanksgiving — and runs with reliable snowpack through to mid-April at the high-elevation resorts. The -10 to -5°C (14–23°F) overnight temperatures that lock in the powder build throughout December, with January and February bringing the deepest and most consistent conditions: daytime temperatures on the mountain runs of -3 to 2°C (27–36°F) under blue Colorado skies that receive, on average, 300 days of sunshine per year as measured across the Front Range by the National Park Service. The Christmas and New Year fortnight is the highest-demand window of the ski year — Aspen, Vail and Breckenridge all book heavily from the American Thanksgiving weekend through to early January, with the period from 26 December through 2 January representing the absolute peak across all three clusters. Owners who can be flexible on exact dates often prefer the first two weeks of January — the crowds thin, the snowpack is building, and the lift queues become a fraction of their holiday-week size. Presidents' Day weekend in mid-February is the second major domestic-demand spike, followed by the March spring-break window, which runs across two to three weeks as different school systems take their mid-semester breaks at different points. Spring skiing in Colorado — late March through mid-April — is a distinct and beloved season of its own: daytime temperatures climbing to 4–10°C (39–50°F) with strong March sun, corn snow by 11 am on the south-facing runs, lunches on the mountain deck, and a significantly mellower social atmosphere than the mid-winter peak. Aspen's Buttermilk and Breckenridge's lower peaks sometimes close before the higher terrain; the expert zones at Vail's Back Bowls and Aspen Highlands remain in excellent spring condition through to mid-April in most years. For owners who ski seriously and can schedule outside the school-holiday windows, the late-season weeks often provide the best combination of conditions and ambience in the ski calendar.

April and May are Colorado's shoulder season — the mountain towns are quiet, the ski lifts have mostly closed (Arapahoe Basin and Breckenridge's upper terrain sometimes run into May), and the transition from ski-resort intensity to summer outdoor recreation is one of the more complete seasonal transformations in any mountain destination. April temperatures run from 0 to 10°C (32–50°F) at resort altitude, with the valley floors below already warming into genuine spring; the wildflower season begins in earnest on the mountain meadows as the snowpack retreats, and the trails open progressively through May. For owners who do not need to align with school calendars — empty-nesters, pre-children couples, owners prioritising the summer cultural season — the April-May window offers the mountain experience without any crowd pressure, with the towns running on their quieter community-focused seasonal cadence. The Roaring Fork Valley below Aspen transitions to fly-fishing season on the Roaring Fork and Crystal Rivers; the Colorado River corridor through Glenwood Canyon reaches its white-water peak as spring snowmelt runs through the canyons. The Glenwood Caverns and the famous Glenwood Hot Springs — a significant community resource for the entire I-70 corridor — are at their most accessible during the shoulder. This is also the period of the Aspen Ideas Festival preview programming and the early events of the Vail lecture and arts calendar before the high summer season begins.

Colorado's summer is, for a significant and growing proportion of fractional owners, as valued as winter — and in some respects more remarkable, because it is less expected. Daytime temperatures at resort altitude run from 18–25°C (64–77°F) in July and August — the famous "Rocky Mountain high" climate of warm dry days, cool nights and afternoon thunderstorm buildups that clear quickly and leave the air crystalline — and the depth of outdoor recreation quality is extraordinary. The high-altitude summer light has a quality unlike any other domestic US destination: strong, clear and long-eveninged, with Colorado Tourism Office data consistently identifying the state's mountain summer as the primary draw for visitors from California, Texas and the Northeast who make the inland journey despite the beach alternative. The Rocky Mountain National Park, accessible from the Vail and Summit County corridors via a scenic two-hour drive through Estes Park, is the fifth most-visited national park in the United States and is at its peak condition in July and August when the wildflower meadows below treeline are in full bloom and the Trail Ridge Road — crossing the Continental Divide at 3,713 m (12,183 ft) — is fully open. Vail's lift-served mountain bike trails operate from mid-June through October, with the Epic Discovery summer activity park running parallel on the slopes. The Aspen Snowmass summer programme combines hiking, biking, fly-fishing, paragliding, horseback riding and river kayaking across the four-mountain network. Breckenridge's summer revolves around the Breckenridge Music Festival (July–August), the long summer hiking trails on Peaks 8 and 10, and the extraordinary wildflower displays on the alpine tundra above treeline that typically peak between mid-July and early August. The cultural peak of the summer is concentrated in Aspen: the Aspen Music Festival runs ten weeks from late June, the Aspen Ideas Festival in late June draws global policy figures and intellectual leaders to the valley, and the Food and Wine Classic in mid-June is the most important event in the American food calendar. For owners who value cultural programming alongside outdoor recreation, summer in Aspen is a uniquely compelling proposition — a world-class music and ideas festival season at altitude, in a mountain town that runs at its most livable during the warm months.

September and October are the months that Colorado insiders consistently name as their favourite — and they are chronically under-booked by fractional owners who default to winter or summer. The reasons are easy to understand from the ground and less obvious from a travel calendar. The aspen-tree season — the annual transformation of the Roaring Fork Valley, the Eagle River corridor and the Summit County mountainsides into a mosaic of gold, amber and russet as the quaking aspens drop chlorophyll — typically runs from mid-September to mid-October and produces a landscape spectacle that draws photographers, hikers and leaf-peeping day-trippers from across the western US. The Colorado Parks and Wildlife manages over 40 state parks with dramatic autumn foliage; the Rocky Mountain National Park, two hours north of Vail via the I-70 and Estes Park, is at its most visitable in September when summer crowds have cleared and the elk rut provides one of the great wildlife spectacles of North America. Temperatures drop steadily through October — 10–18°C (50–64°F) days in early October, 0–10°C (32–50°F) at resort altitude by late October — and the season has a dual character: warm golden afternoons and cold nights that produce the first dusting of early snowfall on the peaks by mid-October. The restaurants in Aspen, Vail and Breckenridge run their full autumn menus without the summer crowds; the ski trails that were mountain-bike routes in August begin to close for grooming in late October; and the world pauses slightly before the winter machine starts again in November. November itself is the pre-season window — the resort towns at their quietest, the early snowpack building, and the first days of inbounds skiing possible at Breckenridge and A-Basin by mid-to-late November in good snowpack years. Owners willing to tolerate patchy coverage for the first turns of the season are rewarded with empty mountain days and a resort-town atmosphere that no other window of the year replicates.

Colorado's mountain second-home market draws from a distinctly international and bi-coastal buyer base that is, in some respects, more diverse than the domestic-dominated narrative of American ski resorts suggests. The dominant domestic cohorts are Texas buyers (Dallas, Houston and Austin, who drive the largest single US-state demand cohort for Breckenridge, Vail and Beaver Creek), California buyers (Los Angeles and San Francisco, with a particular Aspen concentration in the California-to-Aspen migration pattern established in the 1960s), New York and Northeast buyers (New York City, Boston, Washington DC), the Chicago and Midwest market, and the increasingly significant Denver-and-Front-Range permanent-resident market of buyers who want a mountain asset they can realistically drive to on a weekend. The international buyer mix is heavily British and European — a function of Aspen's long Anglo-American cultural relationship and the direct Heathrow-Denver routing by British Airways and United Airlines that makes Denver the most directly accessible US mountain gateway from the UK — plus growing Mexican, Brazilian, Argentinian, Canadian and Australian cohorts across the three major clusters. The post-Brexit Schengen constraint has driven additional British buyers specifically toward Colorado over the past three years.

Fractional ownership in Colorado typically suits:

A pattern worth examining in more detail is the multi-region buyer — Colorado owners who hold a second COP share elsewhere. The single most common combination observed across the portfolio is Colorado plus a warm-weather summer destination: a Vail or Aspen winter share paired with a Mallorca, French Riviera, Italian Lakes or Andalusian coastal share for the June-to-September months when Colorado at altitude is stunning but the Roaring Fork Valley basin can run warm and the beach has its own pull. The second-most-common pattern is Colorado plus a warm-climate US domestic share — a Florida, California or Lake Tahoe-adjacent share for an owner who wants the continental variety without the European time-zone overlay. The third and fastest-growing pattern, observed particularly among British buyers, is Colorado plus a retained European share that is now used under the Schengen 90-day constraint — the owner uses their Schengen days for one or two European visits per year and fills the remaining calendar with Colorado, where there is no day-count pressure. Two 1/8 shares across complementary climates and seasons deliver approximately 90 days of use across a calendar year, drawn from genuinely different lifestyle modes, at a combined annual carry that remains a fraction of what a single whole property at either address would cost. This is the arithmetic that makes the multi-region model compelling at the fractional level in a way that it rarely is for whole-ownership portfolios: the entry level is proportional, the management is parallel, and the LLC consistency means the owner adds a share in the same familiar structure rather than entering an entirely new ownership environment each time.

The buyer profile that Colorado fractional ownership serves least well is also worth naming honestly: owners who can only schedule one or two weeks per year, whose primary constraint is the number of available vacation weeks rather than the cost of ownership, may find that the 6–7 week annual allocation of a 1/8 share is more than they will realistically use over a five-year horizon. In that case, a smaller fractional interest — a 1/12 or a 1/16 share, where available — or a high-quality hotel or rental programme for occasional visits is probably more appropriate than a co-ownership commitment. The fractional model works best for buyers whose ideal use is genuinely in the 4-to-7-week annual range and who want the permanence, the asset ownership, the management simplicity and the resale optionality that a deeded share provides — and who are willing to engage with the LLC operating framework, the annual service charge, and the co-owner relationship that comes with shared ownership. For that buyer, and particularly for the international buyer whose alternative is the complexity of direct US property ownership from another country, Colorado fractional co-ownership offers a genuinely compelling proposition that no other ownership structure in the US mountain market currently matches at the same combination of quality, management simplicity, and international structural consistency.

Denver International Airport (DEN) is the primary gateway for Colorado mountain properties and the fifth-busiest airport in the United States by total passengers, with a geographic position that gives it strong nonstop coverage from every major US hub and an expanding international network. From the UK, British Airways and United Airlines operate year-round direct services from London Heathrow to Denver, with the flight running around 10 hours 15 minutes westbound and 9 hours 30 minutes eastbound. From continental Europe, Lufthansa operates direct Frankfurt–Denver, and the Denver International Airport site lists the current full international route map. The drive time from Denver International to the major resort towns via the I-70 mountain corridor runs as follows: Breckenridge: 1 hour 45 minutes (via I-70 west and Highway 9 south); Vail: 2 hours (via I-70 west to Exit 176); Beaver Creek: 2 hours 10 minutes (via I-70 west to Exit 167); Aspen: 4 hours (via I-70 west and Highway 82 south-east). These times are in normal non-holiday conditions; the I-70 mountain corridor through the Eisenhower-Johnson Memorial Tunnels — at 3,401 m (11,158 ft), the highest vehicle tunnel in the United States — can back up substantially on the Friday evenings before peak weekends and on the Sunday-afternoon returns, and experienced owners schedule their arrivals to avoid those windows. For Aspen and the Roaring Fork Valley, Aspen-Pitkin County Airport (ASE) takes direct seasonal service from Chicago, Dallas, Houston, Los Angeles, New York and San Francisco, reducing the ground-travel time significantly; Eagle County Regional (EGE) serves the Vail-Beaver Creek corridor with seasonal direct service from the major US hubs. Private aviation to both ASE and EGE is well-established and commonly used by owners arriving from the coasts for ski weekends.

The case for a fractional structure in Colorado is most clearly articulated through the side-by-side comparison against both whole ownership and long-term rental — the three realistic options for holding a Colorado mountain second home.

| Whole second home | COP 1/8 fractional share | Long-term rental | |

|---|---|---|---|

| Upfront commitment | Full property value | ~1/8 of the property value | First/last/deposit only |

| Equity in the asset | Full appreciation | ~1/8 of appreciation | None |

| Annual carry | Full property tax, HOA, insurance, management, maintenance | ~1/8 of carry, fully managed | Full rent every year, indefinitely |

| Personal use | Up to 52 weeks (most use 6–10) | ~45 days, professionally scheduled | Defined by lease |

| Operations burden | Owner-managed or hired staff | Fully included | Landlord-managed |

| Time to exit | 6–24 months on the open market | ~1 month on average | End of lease term |

The comparison that Colorado buyers consistently find most instructive is the annual-carry line alongside the time-to-exit line. Owning a whole Colorado mountain property outright means carrying full county property tax (the ad valorem tax assessed annually by the county assessor — Pitkin, Eagle, Summit and Routt counties each publish their millage rates through the Colorado Department of Revenue), full homeowner association fees (which can be substantial in the managed resort communities where the major fractional properties sit), full property and casualty insurance, full snow-removal, landscaping and year-round maintenance in a climate that is genuinely harder on buildings than a sea-level second home, and a full property-management retainer for the months you are not physically present — every year, whether you use the property for two weeks or twelve. A 1/8 fractional share carries proportionally less in every line, fully managed, with the operational burden lifted entirely. Compared to renting a similar property across a comparable number of weeks over a decade, you build real equity rather than burning rent — and the share is yours to sell, transfer or leave to your children. The time-to-exit differential is also material in a market where whole-property liquidity at the top tier is genuinely constrained: a Vail ski chalet or Aspen mountain home at the top price band can sit 12–24 months on the open market before transacting, and the carrying costs through that period — snowploughing alone is a meaningful line item through a Colorado winter — add to the effective exit cost in a way that a fractional exit, typically clearing in around a month or less, avoids.

The annual carry on a 1/8 Colorado share is, by definition, roughly 1/8 of the carry on the equivalent whole property — which means it is a fraction of what an outright Colorado mountain-home owner pays in property tax, HOA fees, insurance, management and maintenance, and a fraction of what year-round long-term rental of an equivalent mountain home would cost. The included items typically run to: county property tax as assessed by the county assessor in Pitkin, Eagle, Summit, Routt or San Miguel county; homeowner association fees in the managed resort communities; property and casualty insurance including winter-weather-specific coverage; the full property management retainer covering staff, scheduling, owner relations and the on-call concierge; cleaning and linen between every stay; seasonal maintenance covering snow removal, roof and deck winterisation, spring de-winterisation, landscaping and summer preparation; HVAC, plumbing and electrical maintenance; utility bills (electricity, heating, internet, security monitoring); and a contribution to the reserve fund for major capital works (roof replacement, boiler, structural). What is typically not included: large capital improvements decided by the LLC's annual meeting and funded via levy; major damage events (typically insured); personal staff costs booked by an individual owner for a specific stay; damage caused by an owner's own use; and high-volume utility consumption during personal stays beyond the standard provision. The key point is that the annual figure is a comprehensive operating budget that keeps the property in active, ready condition year-round — including through the demanding Colorado winter maintenance cycle.

Every Colorado property on COP is held in a purpose-built LLC — the same modern international ownership vehicle used across all COP destinations — in which you and up to seven co-owners hold equal LLC membership interests. The underlying Colorado property is held by the company, with title recorded at the county clerk and recorder's office in the relevant county (Pitkin for Aspen and Snowmass, Eagle for Vail and Beaver Creek, Summit for Breckenridge and Keystone, Routt for Steamboat Springs, San Miguel for Telluride and Mountain Village), and your membership interest is recorded in the company's register and transferred on resale or inheritance through a clean, documented administrative process. You hold a real, transferable equity interest in the underlying Colorado real estate — not a timeshare, not a points club, not a use-right. You participate proportionally in any appreciation in the underlying property's market value, can sell through the professional resale process or to any qualifying outside buyer, and can leave the interest to your heirs under your home jurisdiction's inheritance rules, with US probate considerations handled through the LLC vehicle's international structure.

The mechanics of fractional ownership in Colorado are framed by four things working together: the purpose-built LLC structure used to hold every property on COP, the Colorado county property-tax regime that varies by county but is administered at a relatively clean and predictable standard, the federal FIRPTA framework that applies to international buyers holding US real estate (including LLC interests) and shapes both the purchase structure and the eventual resale, and the county clerk-and-recorder system that registers the underlying property and establishes its documentary record. Understanding these four pieces provides the clarity that transforms a Colorado fractional purchase from an abstract transaction to a well-understood ownership position.

The LLC that holds each Colorado property on COP is a purpose-built company designed for international and multi-party shared ownership. It is registered in Colorado or a related jurisdiction, has a managing officer appointed under the company's governing documents, a register of members recording each co-owner's interest, and an annual general meeting at which the co-owners make decisions on major capital works, budget, and manager performance. The same LLC framework runs across COP's destinations — the United States, the United Kingdom, France, Spain, Italy and elsewhere — meaning an owner adding a Colorado share to an existing European COP share is dealing with the same ownership structure, not a new one.

For a fractional buyer in Colorado, the practical effect is that you become a registered member of the LLC holding the property, with one of eight equal membership interests. The property remains Colorado real estate, recorded at the county clerk and recorder, with the LLC as the legal owner of record; you, in turn, are a legal owner of the LLC. What you hold is a transferable equity interest in the underlying real estate — not a timeshare use-right that depreciates toward zero when the contract expires, not a points-club membership, not a fractional holiday club. This two-step structure provides the consistent international format, the cleaner cross-border inheritance treatment compared to directly deeded shared ownership, and the faster resale path — a transfer of LLC membership is a more direct administrative action than triggering a full Colorado title conveyance through a title company and county recorder.

Colorado operates a property-tax framework that varies by county but is, by US standards, relatively predictable and professionally administered. The ad valorem property tax is assessed annually by each county assessor on the basis of the property's assessed value (a statutory percentage of market value), with the resulting taxable value multiplied by the applicable mill levy to produce the annual bill. In the major resort counties, the assessor's office — the Pitkin County Assessor for Aspen and Snowmass, the Eagle County Assessor for Vail and Beaver Creek, and the Summit County Assessor for Breckenridge — each publish their current assessed-value rates and mill levies transparently. All routine compliance — filing, payment, assessment appeals — is handled by the LLC and its appointed Colorado CPA rather than by individual owners. Colorado's property-tax system does not have the homestead-exemption complexity that characterises Florida or California; the county property-tax compliance is straightforward for an LLC-owned second home, and individual co-owners have no direct filing obligations with the county assessor.

For non-US owners, the most practically important federal tax provision governing a Colorado real-estate investment is FIRPTA — the Foreign Investment in Real Property Tax Act. FIRPTA requires a buyer to withhold 15% of the gross sale price on the purchase of US real property (or an interest in an entity that holds US real property) from a foreign person, and remit it to the IRS on the seller's behalf. For an international fractional buyer, FIRPTA has implications both at purchase (the LLC structure and the way the transaction is documented affects how FIRPTA withholding is calculated) and at resale (where it applies to the seller's proceeds). In practice, the FIRPTA withholding on resale is a timing mechanism rather than a permanent tax cost — the excess withheld above actual tax liability is returned through the seller's US federal tax return — but it requires a qualified US tax adviser familiar with international transactions and FIRPTA to navigate correctly. Every international fractional buyer purchasing through COP is directed to appropriate specialist US tax counsel as part of the purchase process. The LLC structure handles the FIRPTA mechanics at the entity level, which is generally simpler than direct-deed ownership for international buyers.

Once the purchase is complete, a professional management company takes responsibility for all operational aspects of the Colorado property. Your personal weeks — approximately 45 days for a 1/8 share — are allocated through a fair-rotation calendar that distributes peak weeks (Christmas-New Year, Presidents' Day, spring break, July Fourth, mid-August) proportionally across the co-owner group over a multi-year cycle. No single co-owner holds the same peak weeks in perpetuity; the rotation ensures every owner receives a fair share of the highest-demand periods over time. Owners book several months in advance through a defined calendar-request process; the management company coordinates the schedule and handles any change requests. The service charge — paid annually by each co-owner — covers snow removal, roof and deck winterisation, spring preparation, cleaning and linen between stays, property tax payment, insurance, HOA fees, utility management, and the on-call concierge throughout the season. The management team also handles the pre-arrival preparation that makes an alpine property genuinely usable on arrival: the property is warm, the hot tub is running, the refrigerator has been provisioned if requested, and the ski equipment has been organised. Between owner visits, the property is maintained in resort-ready condition — a standard of care that requires year-round engagement in a Colorado mountain climate where spring and autumn maintenance cycles are as important as the winter season itself.

When you decide to exit your Colorado share, a professional resale process is in place. Across COP's portfolio, the typical timeline from listing to completion is around a month or less — well under the 12–24 months that whole-property resale at the top tier of the Colorado market typically takes on the open market. The buyer pool is already familiar with the property, the LLC structure and the management framework; the transfer of LLC membership is a more direct administrative action than a full title conveyance; and the FIRPTA pathway for international sellers is handled through the professional advisers already engaged with the property. For owners who want maximum control over price and process, an open-market sale to any qualifying buyer is always an option — the LLC's governing documents include a right of first refusal for existing co-owners, but the market for quality Colorado mountain shares is well-established beyond the co-owner group. The carrying costs of holding a whole Colorado mountain property through a slow open-market sale — ongoing property tax, HOA fees, insurance, snow removal and management — can add meaningfully to the effective exit cost in a way that a quick fractional exit avoids.

The full mechanics of fractional ownership across all jurisdictions — usage calendars, exit procedures, rental income treatment, insurance, the transfer on death, and the relationship with the management company — are covered in our co-ownership explained guide. For specific Colorado property availability, browse the listings in the property grid above, or join our list for new-property alerts as they come to market.

Questions & Answers

Fractional co-ownership in Colorado gives you a legally deeded 1/8 share of a luxury Colorado mountain property — a ski chalet in Aspen or Vail, a mountain retreat in Breckenridge, or a resort home in Telluride or Steamboat Springs. Each COP property is held in a property-specific LLC. Your 1/8 share is genuine property equity — approximately 45 days in America's premier mountain state per year, at 1/8 the full purchase cost of a genuine Colorado ski address.

Colorado's Rocky Mountain ski resorts — Aspen, Vail, Breckenridge, Telluride — are globally recognised as the world's finest ski destinations outside the Alps. They combine world-class mountain infrastructure, exceptional snow quality (Colorado's champagne powder is among the driest, lightest snow on earth), and year-round mountain town cultures with fine dining, arts festivals, and outdoor recreation that extends well beyond ski season. Aspen in particular — home to the Aspen Institute and a concentration of global business, cultural, and entertainment figures — is one of the most internationally prestigious property addresses in North America.

Your 1/8 share gives you approximately 45 days per year. Colorado mountain properties have two distinct peak seasons: ski season (November–April, with January–March the best snow), and summer (June–September, hiking, mountain biking, music festivals). Many Colorado owners split their usage across both seasons. COP's calendar manages peak ski-week allocations through a fair rotating priority system.

Many of our Colorado properties support short-term rental of unused weeks — and where permitted, it is an excellent way to offset your annual costs. COP's rental programme can list your unused allocated weeks on short-term rental platforms, with income paid directly to you after the platform fee. Many co-owners cover a meaningful portion of their annual service charge through rental income, particularly in high-demand locations.

That said, rental availability varies by location — some areas have local restrictions on short-term lets, and not all properties in our portfolio permit it. Always check the individual Colorado property listing to confirm whether short-term rental is available for that specific home before factoring rental income into your plans.

Aspen, Vail, and Telluride have strict development controls that permanently limit new supply in the most desirable ski-front and town-centre locations. Combined with structural demand from East Coast and West Coast wealth, international buyers, and year-round outdoor recreation appeal, these markets have appreciated strongly over the long term. The fractional model makes genuine Aspen or Vail real estate ownership feasible at 1/8 the capital commitment of full purchase.

When you decide to exit, a professional resale process is in place. The supported resale process runs through the COP owner network — your Colorado fractional share is marketed to an existing audience of qualified prospects already familiar with fractional co-ownership and the LLC structure, and you keep full control over price and timing.

Across the COP portfolio, the typical timeline from listing to completion is around a month or less — well below the 6–24 months that whole-property resales typically take on the open market. Note that some properties have a minimum holding period during the first year — check your specific property details before purchase. Because you are transferring LLC shares rather than real property, exit costs are materially lower than a conventional property sale — no full conveyancing fees, no agent percentage on the full property value, just a straightforward share transfer.

Browse COP's Colorado listings to compare properties across Aspen, Vail, Breckenridge, and other Colorado destinations. Submit an enquiry and a COP specialist will contact you within 24 hours.

Get in Touch

Tell us what you're looking for and one of our co-ownership specialists will be in touch within 24 hours.